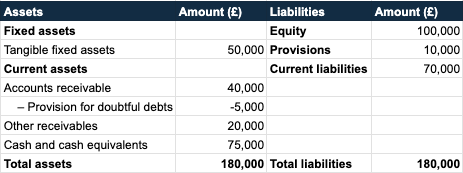

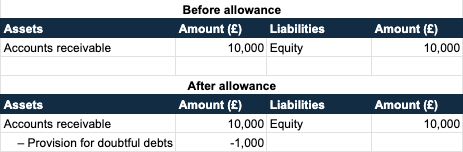

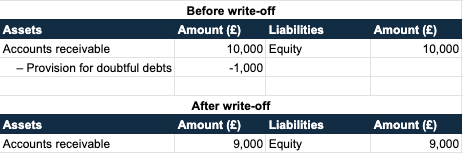

Doubtful debts are customers whose payment of invoices is uncertain. For businesses this is an important concept, as it directly affects cash flow and the annual accounts. In this article you will learn what bad and doubtful debts are, how you record them on the balance sheet and how to handle write-offs in accounting.

Table of contents: